It is not hard to produce a shortlist of financial news headlines for FY2023. Key themes have been repeating throughout the year (and carried forward from the end of 2021/2022):

- Russia Ukraine War – Commencing in February 2022 as a result of the Ukraine’s potential membership in NATO. The reaction from Russia, asserting itself over the former Soviet Union State has turned into a major geo-political crisis and a humanitarian disaster.

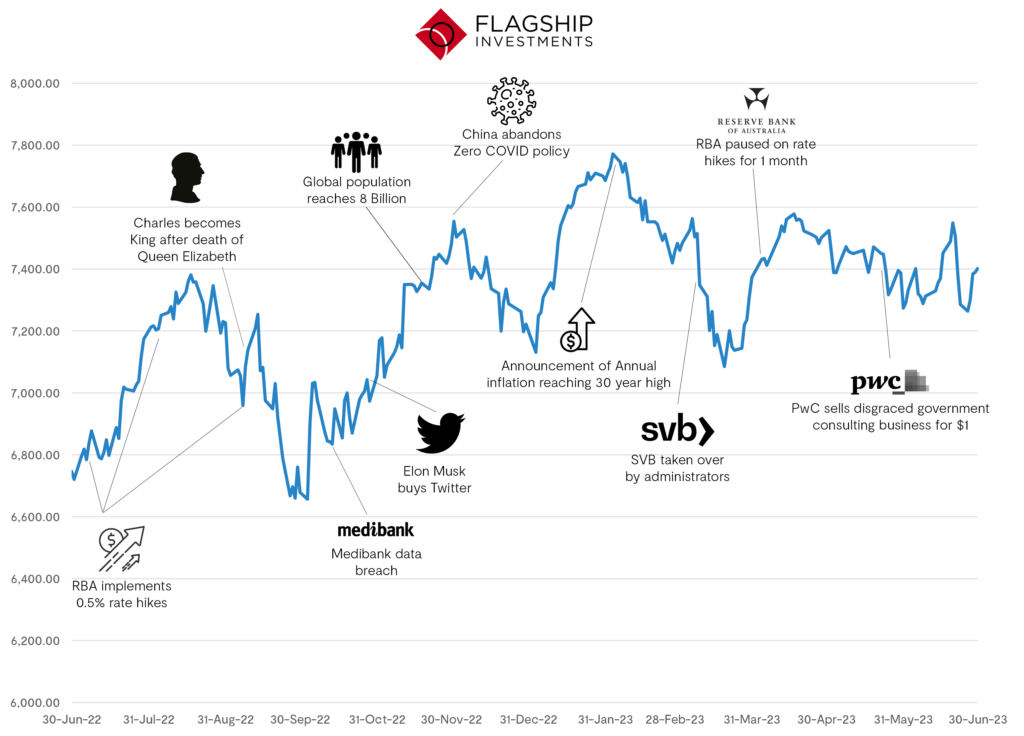

- Widespread Inflation – Supply chain disruption and fiscal policies that stimulated spending have driven inflation worldwide. In Australia the high point reading in December 2022 of 8.4% annual inflation represents a 30 year high, with similar readings globally.

- Interest Rate Moves – Throughout the year central banks have continued to use interest rates to combat inflation. While mortgage holders hope that a pause will be maintained the current rhetoric is that there is still more to come.

- Global economy weakness – with the above items front and centre and slowing growth in many industries the global economy is facing many challenges. In most countries, the talk is about when will a recession occur, not if a recession will occur.

This summary of the macro environment provides a pretty bleak picture, not to mention the recurring news of significant employee layoffs in some of Australia’s best known brands and global tech giants. Yet despite all this negative news the ASX All Ordinaries Index increased by 9.7% for the financial year. This is 5.2 percentage points higher than the 10 year average of 4.5%. And, in amongst this uncertainty the Flagship Investments Ltd Portfolio has performed very well, returning 15.4% for the financial year.

| UNDERLYING PORTFOLIO PERFORMANCE | |||||

| Portfolio^ | |||||

| ASX All Ordinaries Index | |||||

| ASX All Ord Accumulation | |||||

| ^ Source: EC Pohl & Co Pty Ltd Gross performance before impact of fees, taxes and charges. Past performance no predictor of future returns | |||||

The discrepancy between the media focus and the actual performance of the constituents of the ASX All Ordinaries Index is in keeping with the common wisdom that the share market leads the real economy and is an interesting scenario. It will also be interesting to see what reporting season brings now that FY2023 is closed. Annual Reports will be issued before the end of September and management teams will have their opportunity to discuss how the macro conditions have impacted their specific businesses.

One topic that will undoubtedly be discussed during these updates is the use of artificial intelligence (AI) in businesses. Particularly for the investee companies of FSI who are growth stocks and regularly at the forefront of technology adoption. The rise of artificial learning capabilities and applications will certainly be on the agenda. At the last quarterly earnings calls of America’s big tech companies, AI was the centre of attention. At the Alphabet (Googles parent company) meeting AI was mentioned 64 times, Microsoft made 50 mentions and Meta (Facebook’s parent company) made 47 references to the emerging technology.

Novel uses of AI systems are growing, with many people impressed by first draft capabilities in search, coding, copy writing, support centres, artistic creation and other uses. While the applications are broad the results are not always perfect, therefore the output should be considered a first draft rather than a finished product. An exciting prospect is that the use of AI could be the efficiency booster needed to help productivity the same way that personal computers did in the 1980’s. This technology is on a hockey stick trajectory of adoption and improvement, so it will likely look very different in 12 months from today.

For the coming year, inflation readings and interest rates will be an ongoing point of discussion. The perceived mortgage cliff is a possibility given the rate hikes, however housing demand remains strong and it is more likely that discretionary spending is reined in rather than there being a collapse in the housing market. Additionally the unemployment rate remains low, with the business sector still employing despite the economy slowing down. Perhaps this is catchup for latent demand, or perhaps it means some compression in profits in the coming year.

For FSI, the task of monitoring the investee businesses remains paramount. It is the diligent application of the investment process that provides a framework to navigate both the highs and lows of the broader market. We maintain that the process of investing in high quality business franchises that have the ability to generate predictable, above-average economic returns will produce superior investment performance over the long term.