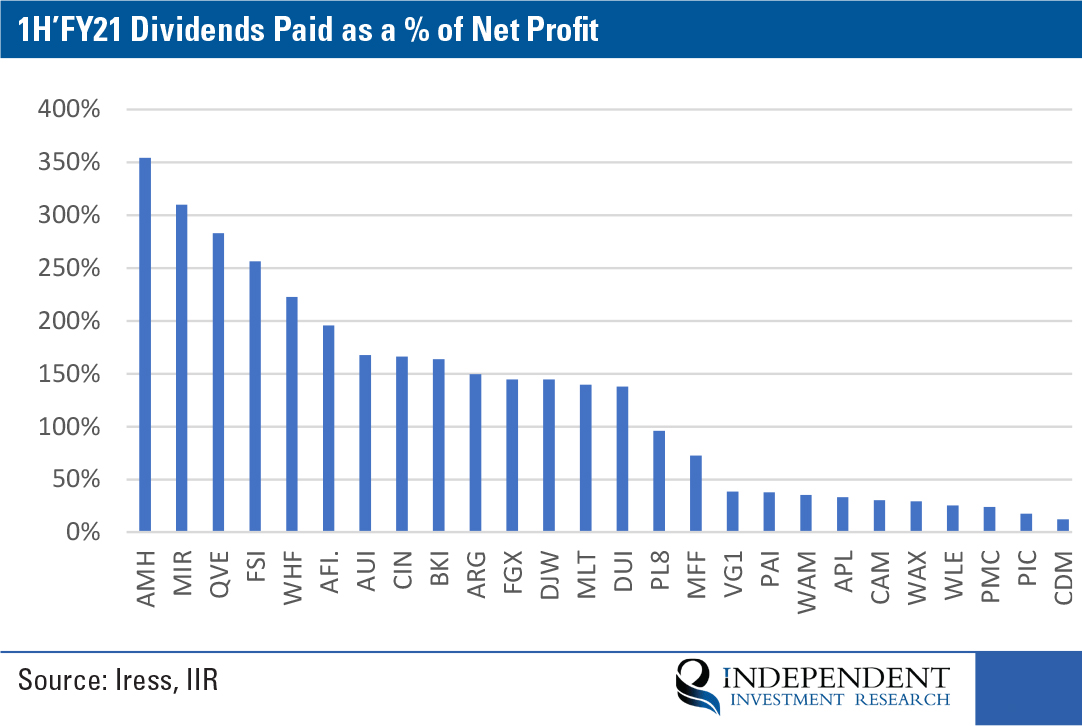

Chart 1: Source IIR. April 2021 LMI Monthly Update

Australian Equity LICs after Covid-19

Now that we have gone a full year since the onset of Covid-19 we are able to review the way that many LICs have managed their dividends through a falling market followed by a sharply rising market. While most have maintained their dividends it is worth looking a little closer to ask how sustainable some of those dividends may be. While we won’t speculate how other LICs will fare going forward it is clear that FSI has a responsible Dividends policy and its payments are supported by long-term strong performance.

In the recently released March quarter LIC/LIT review by Independent Investment Research (IIR) they observed that investors should look closer to ensure that the LIC they have invested in is maintaining a stable dividends policy.

As IIR noted with an estimated (overall) 25% decrease in dividends paid by ASX companies over 2020 it was no surprise that in 1H’FY21 most equity reliant LICs paid out more in dividends than they reported as Net Profit- creating payout ratios greater than 100%, as seen in Chart 1 above. While eyebrows may raise here it should be noted that this was only a 6 month period and many LICs that have low portfolio turnover, may not have generated “book profits” to Dec 31 and some have International Exposure that generates minimal dividends.

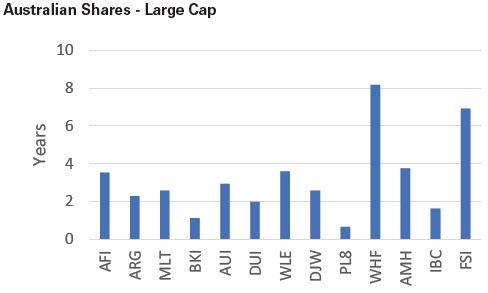

Chart 2: Source IIR. April 2021 LMI Monthly Update: # of Years LIC can maintain current dividend levels given the latest reported retained earnings/profit reserve

Look beyond the headline yield

While the pay-out ratios are interesting, IIR noted that investors should be more interested in the sustainability of Dividends that LICs pay.

As can be seen in Chart 2, were LICs to maintain the same dividend amount, Australian Equity-focussed LICs have on average a little over 3 years of dividend coverage.

Investors in Flagship Investments can take comfort that the dividends the Board makes are responsible, sustainable, and backed by investment performance and it has more than six years of Dividend coverage.

LICs for all stages of the cycle

With the ability to always pay dividends LIC investment managers can focus on investing through the cycle and look for portfolio growth, rather than feeling pressure to generate income from their portfolio to bolster the LICs dividend reserve.

Investors who favour LICs should look beyond the headline historic yield and ensure that its performance has justified and supported the Dividend payments. They should also research how sustainable future dividends may be. While markets go up over the long run there is volatility along the way and any extended declining or even flat market may see some LICs exposed for returning capital and not providing real dividends. What could compound the futility of paying unsustainable dividends is that Boards may have depleted the investment fund size just prior to the market recovery.

LICs that are holding years of reserves will be able to ensure their shareholders continue to enjoy more steady income streams through the investment cycle and the investment manager has artillery (capital) to invest into a rising market.

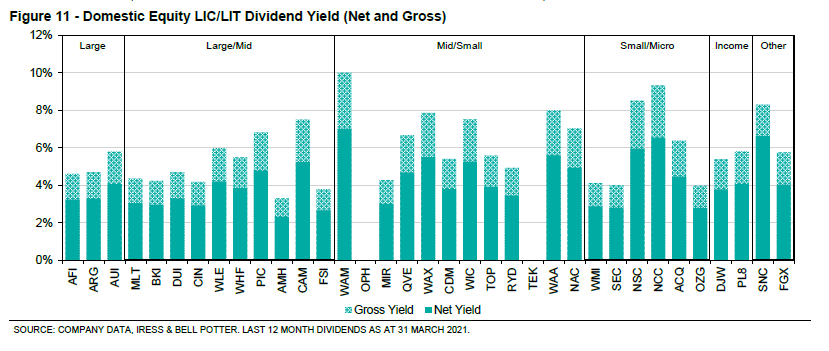

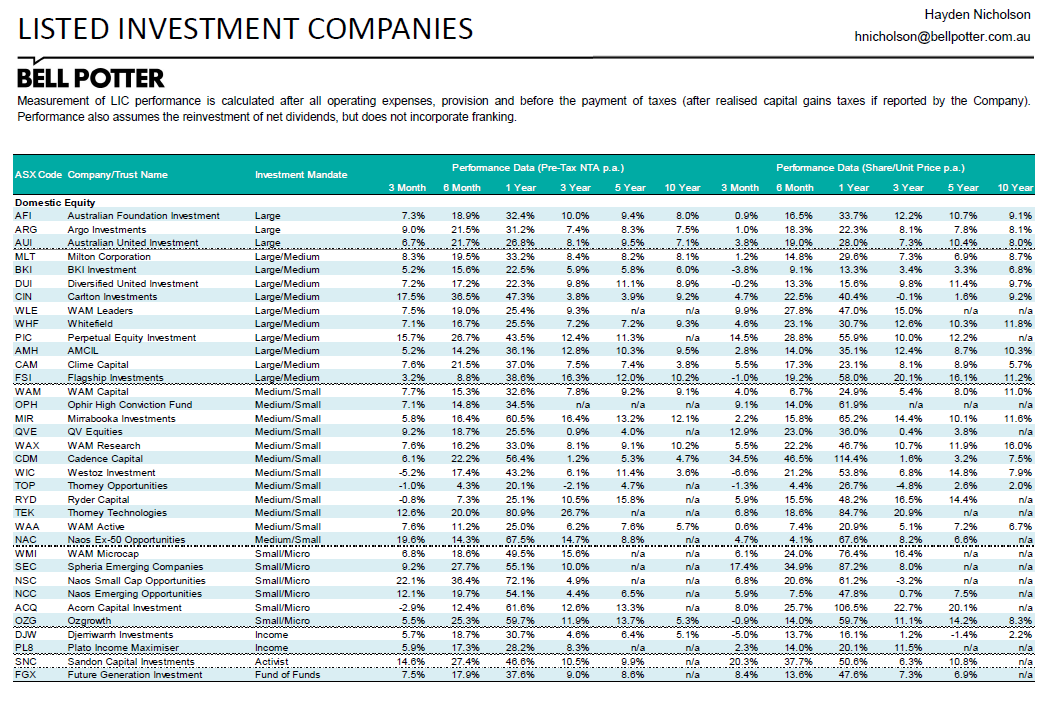

Chart 4: Source Bell Potter. LIC Yield Comparisons

Setting a responsible Dividend policy

The Board of a LIC adds value by declaring the right amount of dividends. Their objective is 3-fold. First to provide shareholders with growing and reliable income streams while Secondly ensuring the strong-performing investment manager is provided with capital to deploy into the market and finally that they are not shrinking the portfolio by simply giving shareholders a dressed-up return of capital.

With this in mind, we can look at the research produced by Bell Potter LIC/ LIT analyst Hayden Nicholson to look at Yields paid by Australian Equities LICs. Readers can look across various data metrics such as Yields paid, dividend reserves, and underlying performance of a LIC to form their own opinion of whether that LICs yield (dividend) has been responsible and is sustainable through a cycle.

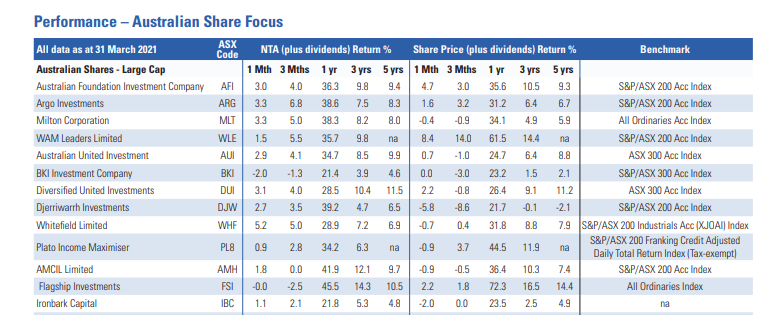

Chart 5: Source IIR. April 2021 LMI Monthly Update: NTA and Share Price performance

Flagship speaks from a position of Authority

Flagship Investments’ objective includes providing shareholders with continued growth in fully franked dividend income. It does this through professional, disciplined management of the investment portfolio and not charging shareholders a management fee – with the manager being remunerated only on a performance basis.

In this performance table produced by IIR, we can see that FSI is a stand-out performer in both NTA growth and Share Price return.

Chart 4: Source Bell Potter. LIC Yield Comparisons

Extending this performance to the most current Bell Potter report dated 11 June 2021, which also looks at the 10-Year performance we see extended FSI performance and outperformance.

Flagship Investments Limited (ASX: FSI) has been a strong performer since it first listed in December 2000.

The Market recognises Flagship performance

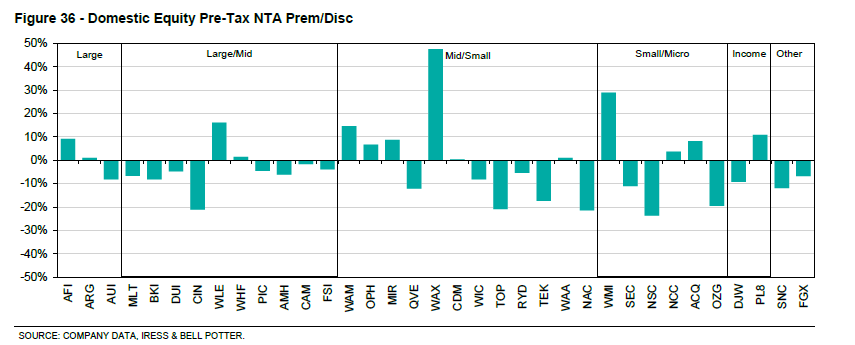

Chart 7: Source Bell Potter. LIC Yield Comparisons

In the Bell Potter LIC March quarter report respective Pre-Tax Premiums and Discounts are plotted within each LICs area of investment focus. FSI can be seen as near parity to its share price.

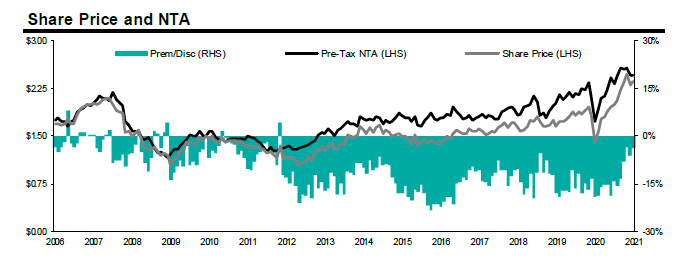

Chart 8: Source Bell Potter. FSI Share Price and NTA growth

Considering its long-term profit that was generated by strong portfolio performance, its outperformance to the market and peers, a constant and responsible dividend, and its record high NTA and Share Price this would be of no surprise to FSI shareholders.

Positive forward sentiment

In recent investment commentaries the investment manager of the FSI portfolio Dr Manny Pohl, AM, has continued to indicate a positive sentiment towards the markets. Articles and Interviews with Dr Pohl and the investment team can be read and watched through the Flagship website and also the Investment Manager’s website.

Shareholders can have confidence in the ability of the manager to continue its strong performance and the board to deliver rewarding and responsible dividend outcomes.

Important Note and Disclaimer

This article is provided for educational purposes only and should not be considered as financial advice. Please consult professional advice before making any investment decisions.