In the last six months, the phrase “new normal” has come to encapsulate the transformative changes affecting every aspect of daily life. Since the world was introduced to COVID-19, countless routines and activities have been disrupted, cancelled, or reimagined in the name of public health and safety. As the financial year draws to a close, we are left to ponder: is this our new way of life, or is there more change on the horizon?

Impact on Financial Markets

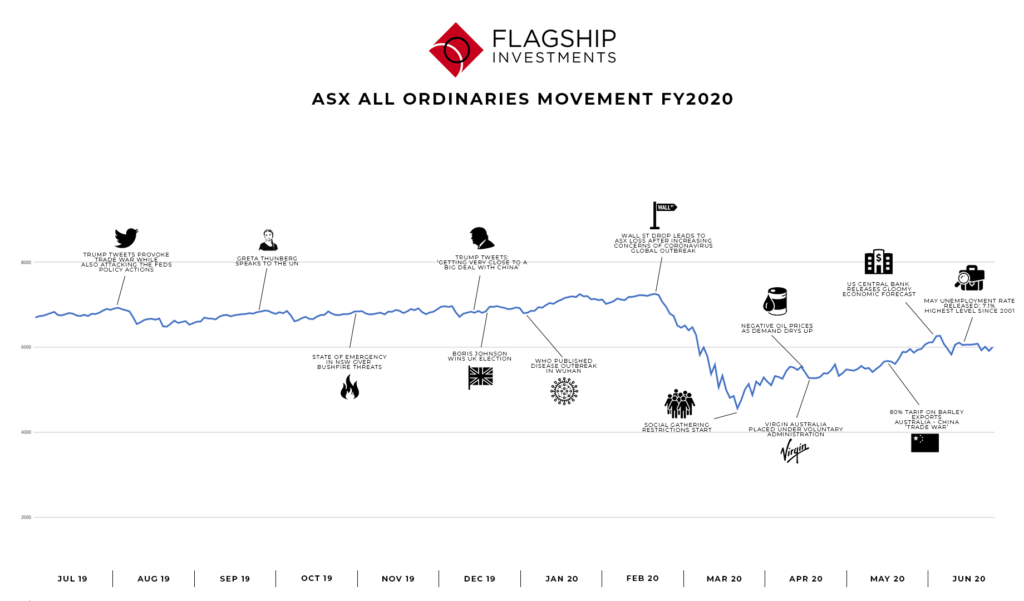

The impact of COVID-19 on financial markets has been nothing short of dramatic. Every major index has experienced significant downturns, and the ASX All Ordinaries is no exception. As illustrated in the attached graph, the index initially reflected forecasts of moderate growth without upward pressure on inflation.

In December 2019, there was a sense of excitement and relief following positive developments in the US-China trade war and the Brexit deadline set for 31 January 2020. During the first two months of 2020, the index gradually climbed higher until the Wall Street drop on 21 February triggered a sharp decline in the ASX All Ordinaries. For insights into the performance of the ASX All Ordinaries and how it has been affected by recent events, refer to the Performance page.The rapid spread and impact of COVID-19 heightened concerns among nations and markets alike, as businesses began to signal potential earnings growth challenges. It became increasingly clear that this would be a significant global event.

ASX All Ordinaries Movement FY 2020. Click to expand.

The Advantages of Unfranked Dividends

In response to the COVID-19 pandemic, governments around the world took decisive action, prioritising medical and safety considerations. A series of social distancing restrictions were implemented, followed by financial stimulus packages aimed at mitigating the impact on business viability and household incomes. For a deeper look at why unfranked dividends might be advantageous, see Franked vs Unfranked Dividends: Which is Better. As schools, shopping centres, and hospitality outlets closed, many people adapted to working from home and increased their hygiene practices, often sanitising their hands every 15 minutes.

Market Reaction

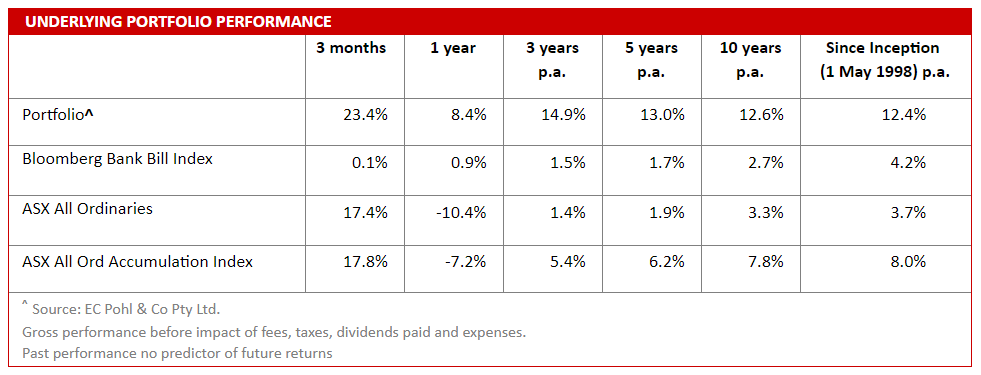

The market’s reaction to these distancing measures was dramatic. The All Ordinaries index rebounded by 12.5% just three days after hitting a low point on 23 March 2020. As COVID-19 cases began to decline, the index continued to rise, ultimately closing at 6001.3—31.5% above the March low, though still reflecting a 10.4% decrease for the 2019/2020 financial year. While these quarterly gains provided some reassurance to investors, those simply tracking the index would have experienced short-term losses. In contrast, the Flagship Investments portfolio rose by 31.8% during this volatile period and increased by 8.4% over the entire financial year.Long-Term Perspective

However, we emphasise that this is merely a short-term view. We prefer to evaluate performance over five-year and ten-year periods, as well as since inception, to better assess the long-term value of our investments.

Underlying Portfolio Performance. Click to expand.

There remains considerable uncertainty about what the future holds, and we anticipate that volatility will continue. On a positive note, the stimulus measures may have been sufficient to keep businesses afloat, allowing consumption and earnings to rebuild and grow back to previous levels as restrictions are lifted.

Conversely, the stimulus has been likened to a Kugel Fountain – a steady flow of money that supports businesses and markets. However, if this flow is cut off, we could see a dramatic decline, with significant consequences.

Time will reveal which perspective holds true. Historically, challenges have eventually led to improvement. At Flagship Investments, our priority remains focused on the long-term earnings potential of our investee businesses. We believe that even during turbulent times, high-quality, sustainable businesses with a competitive advantage will deliver superior investment returns over the long term. In this sense, the “new normal” mirrors the “old normal.”