Listed over 2 decades ago Flagship Investments Limited LIC (ASX:FSI) keeps on keeping on – generating wealth for its shareholders.

In the June 2021 Quarter Review from Hayden Nicholson, LIC researcher for Bell Potter Limited, FSI was noted as having the highest Large Cap Australian Equity returns over 3 and 5 years for both its NTA performance and Share Price return. A closer look at FSI and other LICs demonstrates that FSI offers a point of diversification and differentiation from those more widely recognised LICs and should be considered for inclusion in investors’ portfolios.

Table-topping Performance

Chart 1. Source: Bell Potter. NTA performance (Red highlight added by this author)

As is apparent in Chart 1 below FSI is the best performing Large-cap LIC by NTA performance over 3 and 5 years. This performance demonstrates the superior stock selection skills of the investment management team.

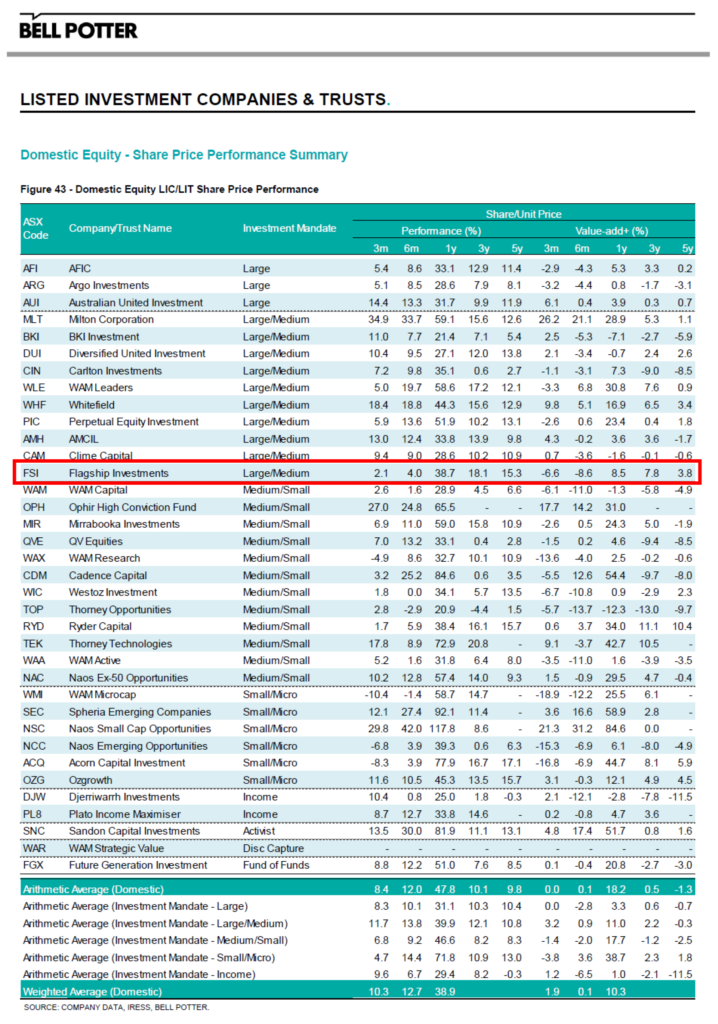

Chart 2. Source: Bell Potter. Share Price Performance. (Red highlight added by this author)

Not only is FSI the best performer by NTA performance but as shown in Chart 2 it has also delivered its shareholders the highest Share Price return over both 3 and 5 years – again demonstrates that it is a standout LIC for its shareholders.

FSI speaks from a position of authority FSI for Diversification

Chart 3. Source: Bell Potter. 5 Year monthly NTA correlation between Large Cap Australian Equity LICs. (Yellow highlight added by this author with permission)

The Bell Potter research report has offered a previously not seen insight into the correlation between various Australian Equities LICs and these are shown in Chart 3.

FSI, seen at the bottom, has a lower correlation to these other LICs. Further, other LICs recognised as being the traditional “big-guns” of the LIC space can be seen to have a higher correlation to one another. An argument can be made that they are almost indistinguishable. Investing in more than one of these may not provide much diversification, risk protection, or opportunity to generate excess performance.

This would be even further amplified if you already held many large-cap stocks directly and then invested in these high-correlation LICs. You could be “tripling up” and incurring unnecessary direct cost and opportunity costs. Also, don’t forget that your super fund probably has a large allocation to these same stocks too. FSI on the other hand has a lower correlation to all the other Australian Equity large-cap LICS and is clearly differentiated, offering potential investment diversification.

[NB It should be noted that the other lower correlation LICs in this table in CIN and PIC are specialist LICs: PIC is ¼ international holdings and CIN holds nearly 40% of its portfolio in just the 1 stock – Event Hospitality and Entertainment Ltd.]

FSI performance is clearly through superior stock selection

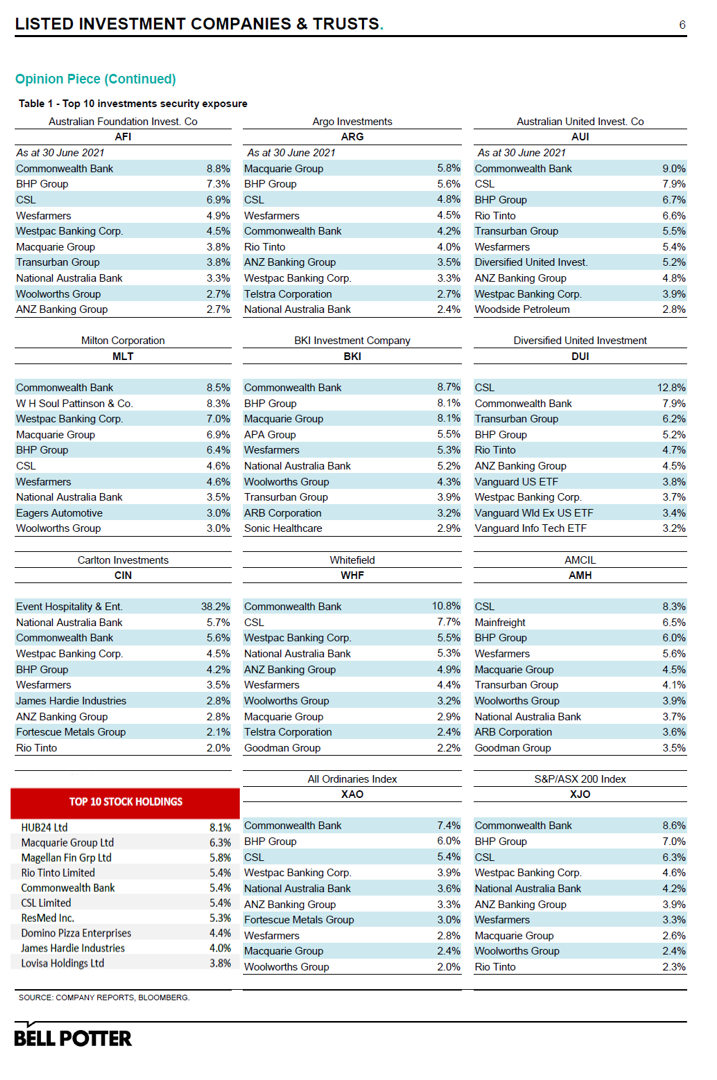

Chart 4. Source Bell Potter. Top 10 positions of selected Australian Equity LICs (with FSI top 10 holdings superimposed at bottom left corner for comparison with chart author’s permission)

If we look through at the top 10 stocks held by the giant LICs – which represent almost all of all money in Australian Equities LICs – shown in Chart 4, we can see that they are virtually indistinguishable to each other. It is hardly surprising that their correlations are high.

FSI on the other hand proves the value of a disciplined process in portfolio construction. As we compare FSI’s top 10 holdings (see bottom left of Chart 4) to those of the other LICs we see unique names.

In light of FSIs lower correlations, it is not unsurprising that its largest and 3rd largest holdings, HUB24 and Magellan Financial Group are not seen in any of the top 10 holdings of these other LICs. Looking deeper across FSI’s top 10 holdings we can see that of 4 more positions (Resmed, Domino Pizza, James Hardie and Lovisa Holdings) only 1 of these can be found, once (James Hardie) in any of these other LICs top 10s.

FSI performance is clearly through its superior stock selection.

FSI holdings are differentiated

Chart 5. Source Bell Potter. Sector Weightings for selected Australian Equity LICs and Indexes. (with FSI Sector Weighting superimposed at bottom left corner for comparison with chart author’s permission)

It is important to also look beyond the top 10 positions in these highly correlated LICs to explore the rest of these LICs portfolios.

Considering AFIC and Argo for example are each charging their shareholders in excess of $11m* each year to manage their investment portfolio it can be asked what they are doing to generate outperformance and earn their fee. (*AFIC $9.54 billion market cap and a management fee of 0.13% = $12.4m and Argo $6.47 billion market cap and a management fee of 0.18% = $11.7m)

One insight into this is to examine the Sector Weightings for each of these LICs, which can be seen in Chart 5 below where FSI has been superimposed into the bottom left corner by this author for quick comparison. Doing so we can clearly see FSI is different to other LICs and the All Ords and ASX200 indexes.

While in Chart 5 we see some uniqueness between these LICs emerge it is still clear that they are in the main heavily loaded towards Financials, Materials, and Industrials. If you are looking for “stocks of tomorrow” to creep into those portfolios you are probably not going to find too many.

Further, if you are already holding a basket of the top 20 ASX stocks directly or even in your Super fund you should consider what you are obtaining by investing in a LIC whose portfolio closely resembles the indexes. For instance, is there value gained by investing in such a LIC that charges shareholders millions in annual management fees when you could do that yourself by buying a virtually fee-free ETF that replicates the top 20 stocks?

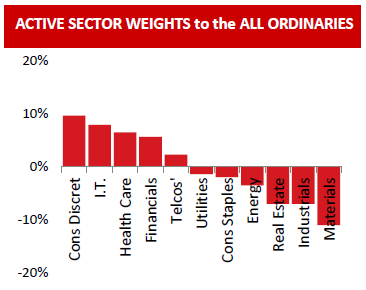

Chart 6. Source FSI Quarterly Shareholders report

Exploring FSI’s active Sector allocation

Looking at the active sector weighing of FSI we can see the uncorrelated nature of FSI is again apparent.

Summary

FSI is distinguishable from other large-cap Australian Equity LICs by its performance on both an NTA and Share Price return basis where it is a table-topping LIC. While many Large Cap Australian Equity LICs are barely distinguishable to one another FSI presents itself for consideration of portfolio inclusion due to both its performance and also it being a differentiated portfolio to other LICs, the index and those household name stocks many investors may already hold. FSI performance has not come by luck but through superior stock selection. It is no surprise that for over 20 years FSI has been recognised for being a leading investor and identifier of what often become the “stocks of tomorrow” and market darlings.

Disclaimer and important note

This article is provided for information purposes only to stimulate the reader to undertake their own research into various investment companies and products. Investors should not rely on this article which does not take into account any person’s particular investment objectives, financial resources or other relevant circumstances, and the opinions and recommendations in this article are not intended to represent recommendations of particular investments to particular persons. All securities transactions involve risks, which include (among others) the risk of adverse or unanticipated market, financial or political developments. Past performance is no guarantee of or predictor of future performance.